Please wait as we load hundreds of rigorously documented facts for you.

Please wait as we load hundreds of rigorously documented facts for you.

For example:

* As defined by government agencies and academic publications, government “social spending” pays for programs that provide healthcare, income security, education, nutrition, housing, and cultural services.[1] [2] [3] [4] [5] [6] [7] [8] [9]

* From broadest to narrowest, some measures of government social spending are:

|

Measure |

Latest Data |

Source |

Portion of Government Spending |

|

|

Federal |

Federal, State & Local |

|||

|

1995 |

U.S. Social Security Administration |

58%[10] |

||

|

2021 |

White House Office of Management & Budget |

71%[11] |

||

|

2020 |

Just Facts (based on the sources above and below) |

73% |

68%[12] |

|

|

2020 |

U.S. Bureau of Economic Analysis |

55% |

46%[13] |

|

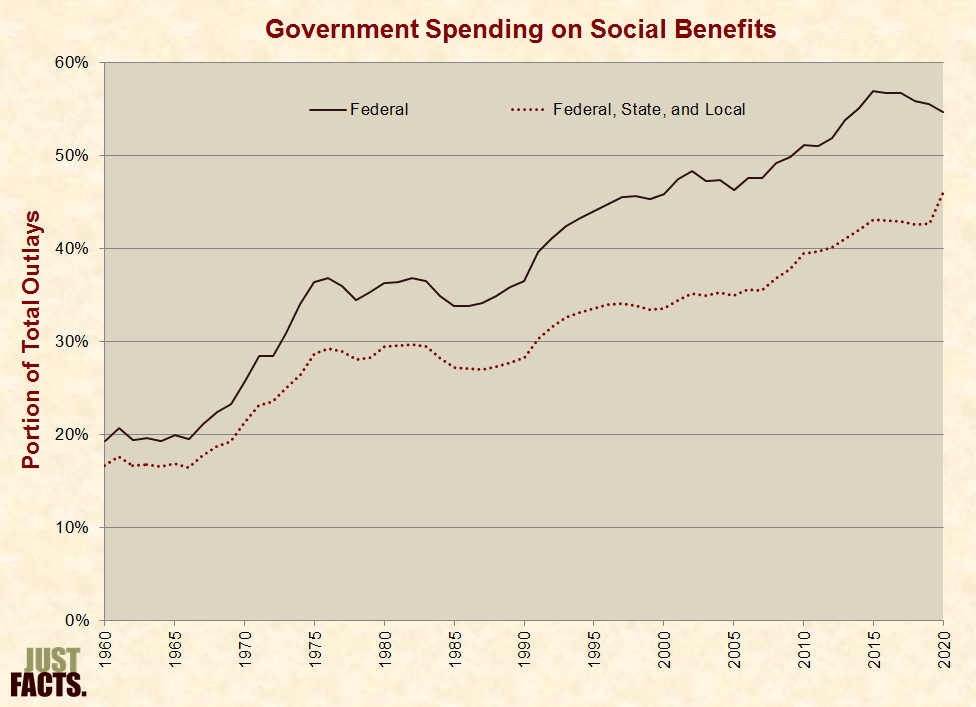

* From 1960 to 2020, the portion of government outlays consumed by various measures of social spending increased by 2.2–3.5 times:

* During 2020 and early 2021, federal politicians enacted six “Covid relief” laws that will cost a total of about $5.2 trillion over the course of a decade. This amounts to an average of $40,444 in spending per U.S. household.[15]

* “Social welfare expenditures”—a measure of social spending published by the U.S. Social Security Administration until 1995—includes:

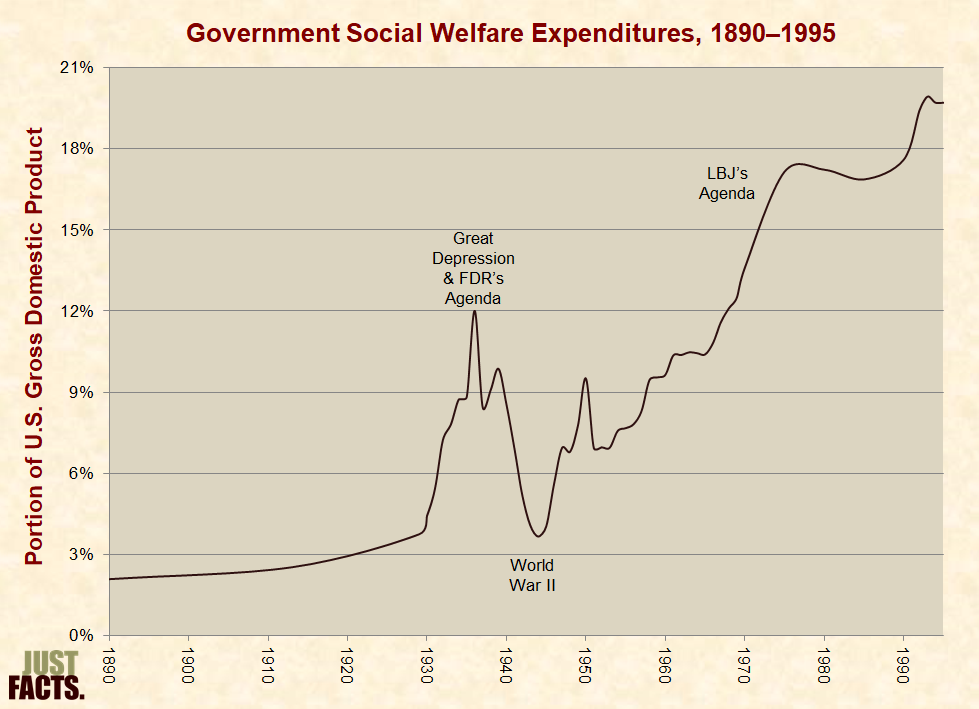

* During 100+ years for which data on social welfare expenditures are available, the following factors had major impacts on such spending:

* From 1890 to 1995, government social welfare expenditures increased from 2% of the U.S. economy to 20%:

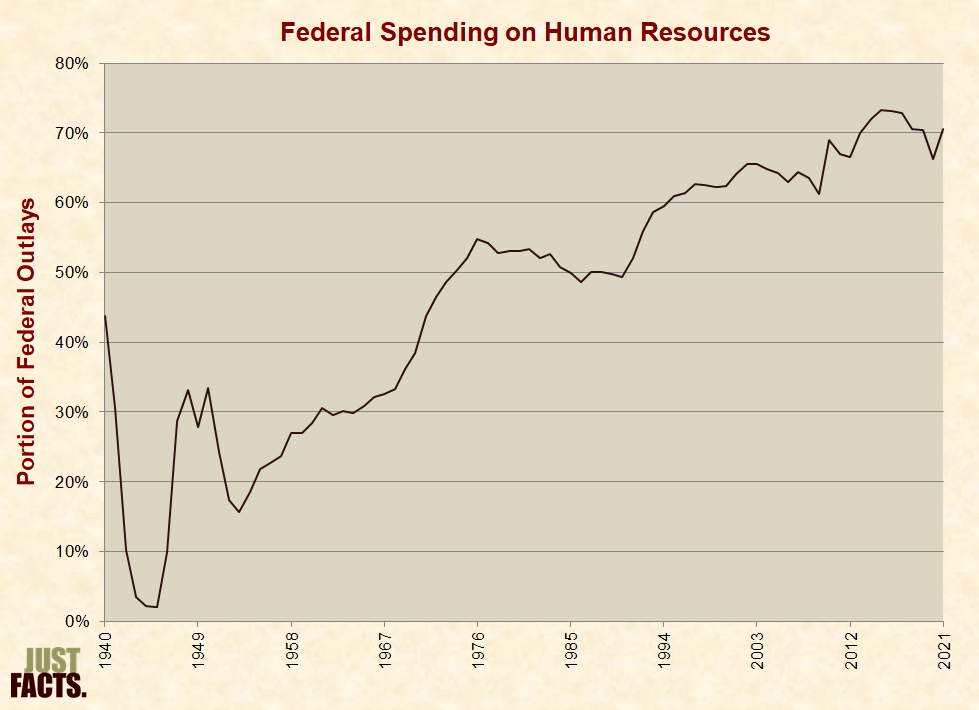

* “Human resources”—a measure of social spending published by the White House Office of Management & Budget—includes spending on:

* This measure does not include spending on the Covid-19 Paycheck Protection Program and certain other pandemic spending programs.[38]

* In 2021, the federal government spent $4,808 billion on human resources.[39] This amounts to:

* From 1940 (shortly after the Great Depression[44]) to 2021, spending on human resources increased from 44% of all federal outlays to 71%:

* “Social programs”—a measure of social spending published by Just Facts based on data from the U.S. Bureau of Economic Analysis and White House Office of Management & Budget—includes:

* This measure does not include:

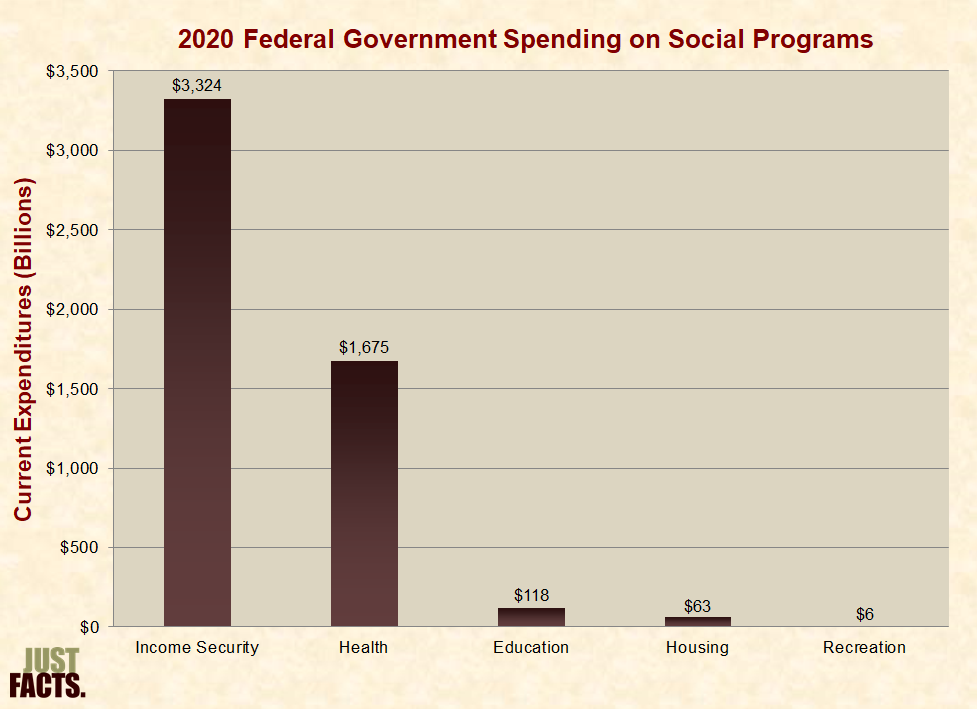

* In 2020, the federal government spent $4,966 billion on social programs.[54] This amounts to:

* In 2020, federal government spending on social programs was comprised of:

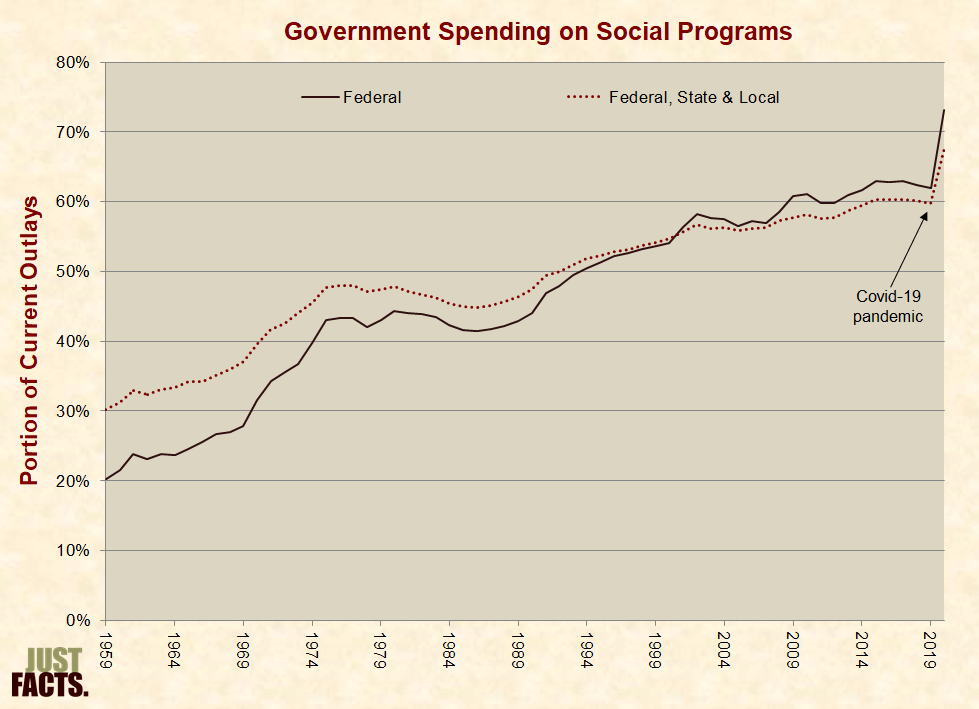

* In 2020, federal, state, and local governments spent $6,054 billion on social programs.[60] This amounts to:

* From 1959 to 2020, spending on social programs increased from:

* “Social benefits”—a measure of social spending published by the U.S. Bureau of Economic Analysis—includes:

* This measure does not include:

* In 2020, the federal government spent $3,785 billion on social benefits.[84] This amounts to:

* In 2020, federal, state, and local governments spent $4,214 billion on social benefits.[89] This amounts to:

* From 1960 to 2020, spending on social benefits increased from:

* Each year, the U.S. government issues a “Publication of Assistance Listings” that provides a “compendium of federal programs, projects, services, and activities that provide assistance or benefits to the American public.”[95] The 2021 Publication of Assistance Listings is 3,877 pages and describes 2,268 programs.[96]

* Some programs in the Publication of Assistance Listings that serve social purposes are not included in various measures of social spending. Examples of these include certain types of environmental initiatives, affirmative action programs, and corporate subsidies.[97]

* “Means-tested welfare” programs provide cash and other benefits to people with incomes and/or assets below certain thresholds. Examples of these include:

* In 2015, the U.S. Government Accountability Office identified 82 federal means-tested welfare programs.[103]

* Seven of the 10 largest federal means-tested welfare programs are “mandatory.”[104] [105] [106] This means they are often funded by laws that require spending to continue indefinitely unless Congress and the president pass new laws to change the status quo. In contrast, Congress and the president typically fund “discretionary” programs for one year at a time.[107] [108]

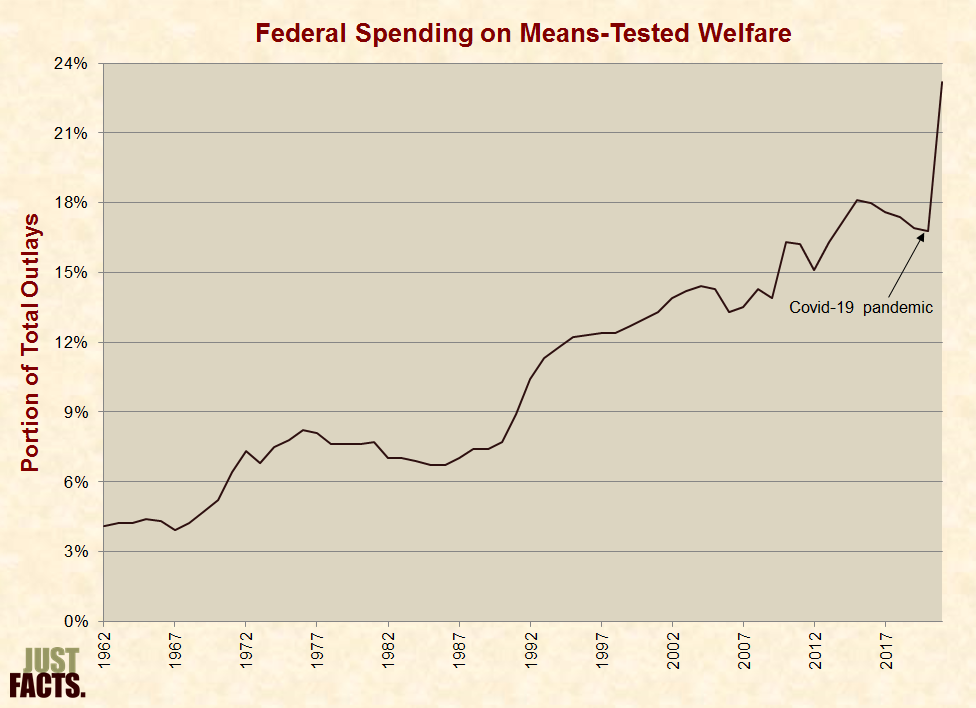

* In 2021, the federal government spent $1,583.6 billion on means-tested welfare.[109] This amounts to:

* In notes that Thomas Jefferson wrote in the 1780s, he described how Americans cared for each other if they became poor or sick:

* In the 1830s, a French historian and political scientist named Alexis de Tocqueville visited the U.S. and wrote a famous work entitled Democracy in America.[117] In it, he stated that what “I most admire in America” is how people were personally engaged in advancing the welfare of society:

* Federal, state, and local government social welfare expenditures were:

* From 1968 to 2004, average inflation-adjusted federal, state, and local government spending per U.S. resident on means-tested welfare multiplied by more than four times.[131]

* From 1962 to 2021, spending on means-tested welfare increased from 4% of all federal outlays to 23%:

* Current government “social insurance” programs in the U.S. include:[135]

* Social insurance programs generally have the following characteristics:

* In 1932 during the Great Depression, the state of Wisconsin created the nation’s first unemployment insurance program.[147] [148]

* Later in the 1930s, as the Great Depression continued, the federal government began creating social insurance programs under Democratic President Franklin Delano Roosevelt (FDR). These programs were modeled primarily after European social welfare programs that began in Germany under Otto von Bismarck, a forefather of National Socialism (a.k.a Nazism).[149] [150] [151] [152] [153]

* In 1941, Luther Gulick, one of FDR’s economic advisors, told FDR that a national sales tax was an economically sounder way to fund Social Security than payroll taxes. FDR replied:

* In keeping with FDR’s political calculus, some people believe that Social Security and other social insurance programs save their payroll taxes for them, and thus, they have a right to the benefits.[155] [156] [157]

* Per the Social Security Administration:

* In 1960, the U.S. Supreme Court ruled (5 to 4) that entitlement to Social Security benefits is not a contractual right.[159]

* Social Security is mainly a “pay-as-you-go” program, which means that it pays most of its benefits by taxing people who are currently working.[160] [161] [162] Per the Social Security Administration:

* From the start of the Social Security program in 1937 through the end of 2021:

* Per the Social Security Administration:

* After the federal government pays back with interest all of the money it has borrowed from Social Security, the program’s current claim against the earnings of future generations is $45.7 trillion. This is larger than the national debt and amounts to an average of $254,931 for every person who paid Social Security payroll taxes in 2021.[166] [167]

* Medicare payroll taxes and the interest they generate funded 34% of Medicare’s outlays during 2021.[168]

* After the federal government pays back with interest all of the money it has borrowed from Medicare, the program’s current claim against the earnings of future generations is $47.8 trillion. This is larger than the national debt and amounts to an average of $183,614 from every U.S. resident aged 16 or older.[169] [170]

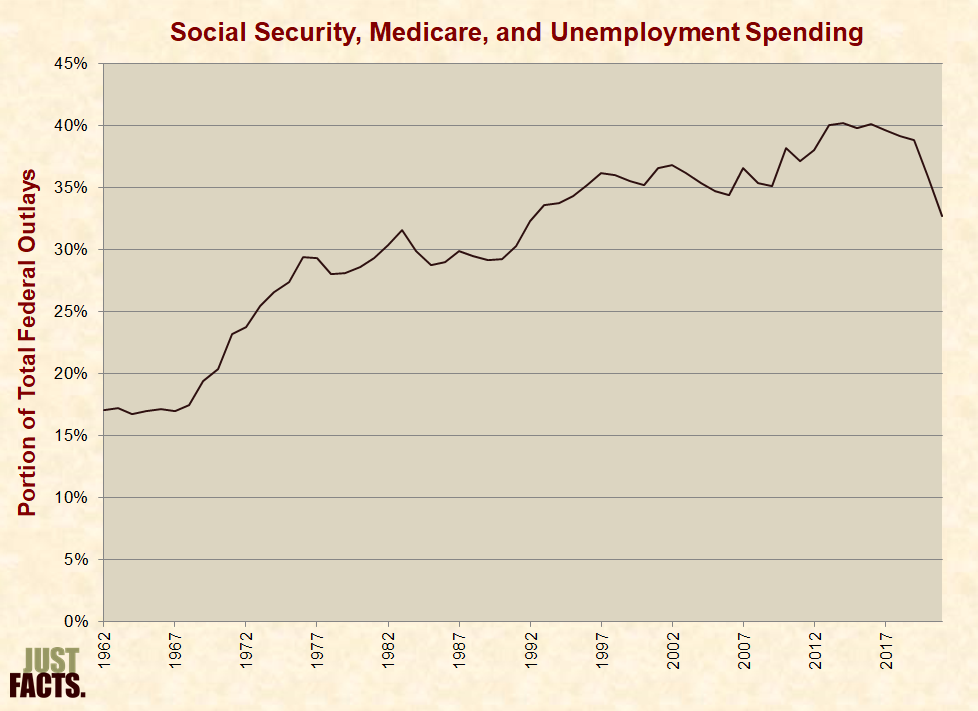

* In 2021, the federal government spent $2,227 billion on the three most-costly social insurance programs (Social Security, Medicare, and unemployment).[171] [172] This amounts to:

* From 1962 to 2021, spending on the three largest social insurance programs increased from 17% of all federal outlays to 33%:

* The largest federal healthcare programs are:[178]

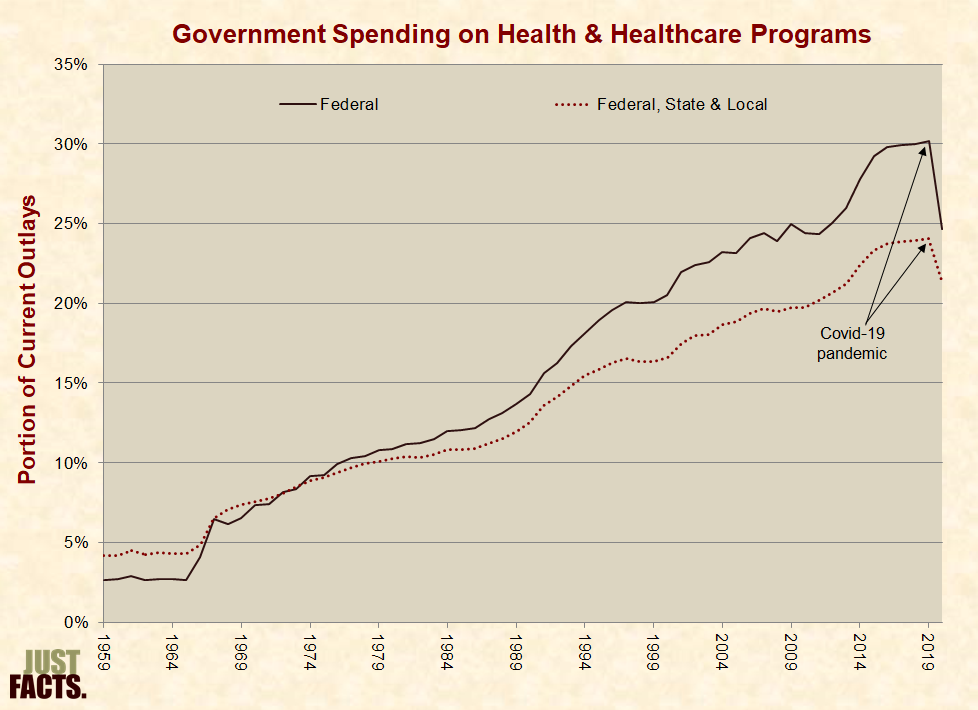

* In 2020, federal, state, and local governments in the U.S. spent $1,900 billion on health and healthcare programs.[186] This amounts to:

* From 1959 to 2020, spending on health and healthcare programs rose from:

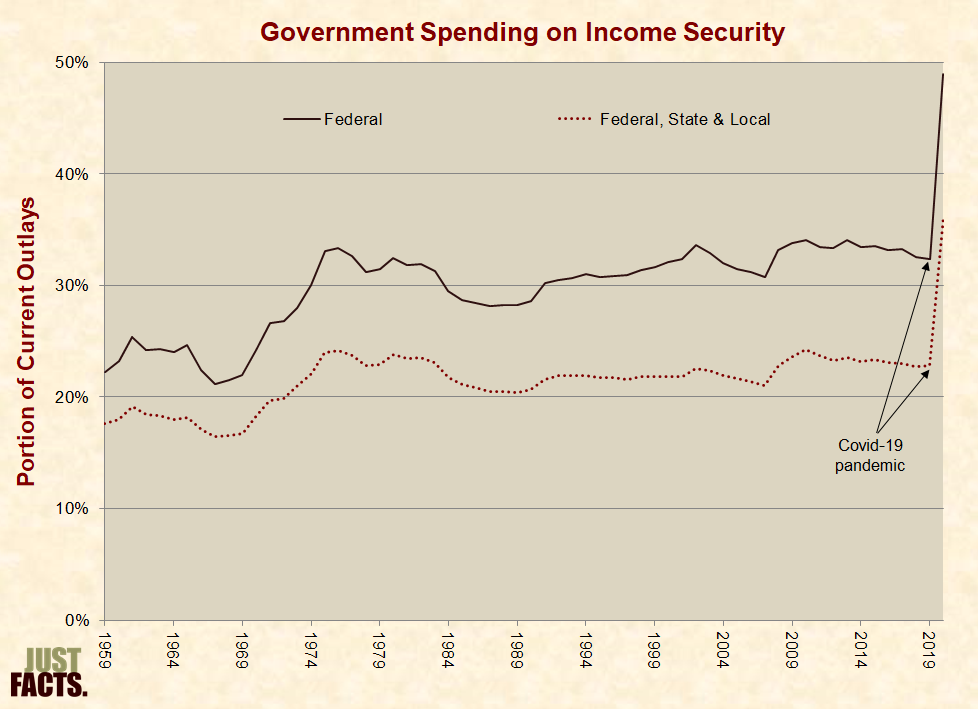

* Government income security programs include a mix of social insurance and means-tested welfare programs, such as:

* In 2020, federal, state, and local governments in the U.S. spent $3,236 billion on income security.[201] This amounts to:

* From 1959 to 2020, spending on income security increased from:

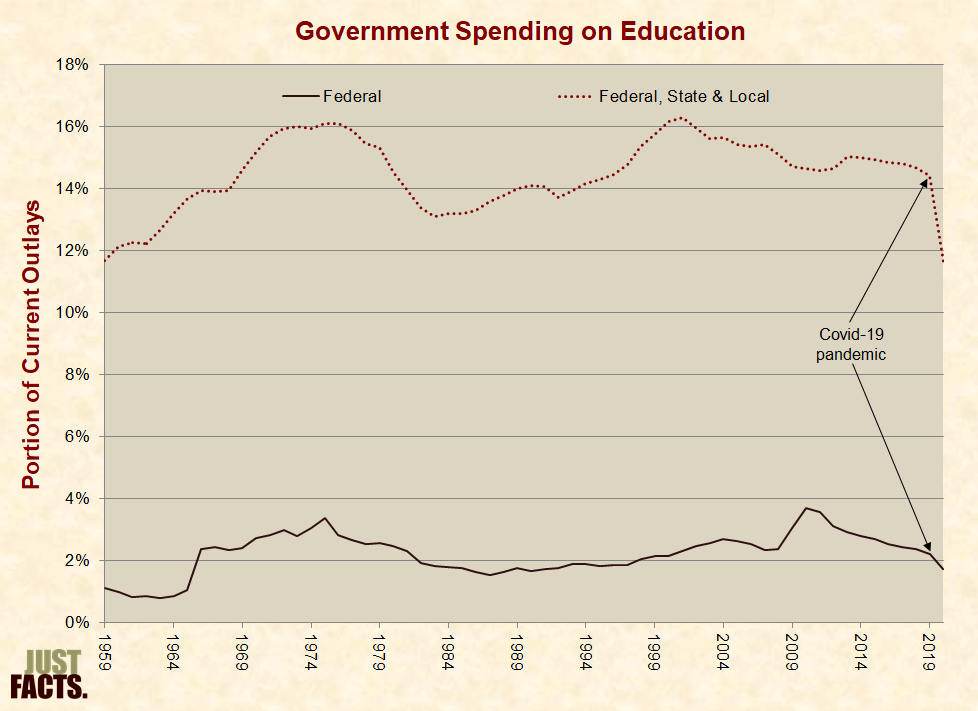

* In 2020, federal, state, and local governments in the U.S. spent $1,036 billion on education.[209] This amounts to $8,069 for every household in the U.S.,[210] 5.0% of the U.S. gross domestic product,[211] and 12% of government current expenditures.[212] [213] These figures do not include:

* Government education spending in 2020 was comprised of:

* From 1959 to 2020, spending on education increased from:

* For more facts about education spending, visit Just Facts’ comprehensive research on education.

* Tax preferences are provisions of the tax code that reduce taxes for certain people in certain cases.[227]

* Per the U.S. Joint Committee on Taxation, tax preferences are “usually … designed to encourage certain kinds of economic behavior as an alternative to employing direct expenditures or loan programs to achieve the same or similar objectives.”[228] [229]

* Many tax preferences have the same effects as government spending. For example, if the government were to repeal the child tax credit and instead send checks to households with children, the effective result would be the same.[230] [231] [232] [233]

* Per the Organization for Economic Cooperation and Development:

* Some tax preferences are refundable, and low-income households with tax credits that exceed their income tax liabilities receive the difference as cash payments from the federal government.[235] [236] [237] [238]

* Due to refundable tax credits, the lowest-income 20% of U.S. households paid an average effective federal income tax rate of –6.6% in 2019 prior to the Covid-19 pandemic.[239] This amounted to an average payment from the federal government of $2,600 per household.[240] [241] [242] [243]

* Due to refundable tax credits, the lowest-income 20% of U.S. households paid an average effective federal income tax rate of –14.2% in 2020—amid Covid-19 government lockdowns and intensified social spending.[244] [245] [246] This amounted to an average payment from the federal government of $6,000 per household.[247] [248] [249] [250]

* With regard to tax preferences, a report by the IRS’s Taxpayer Advocate Service states that the “IRS no longer is just a revenue collection agency but is also a benefits administrator.”[251]

* For more facts about this issue, see Just Facts’ research on tax preferences.

* Though not typically recorded in the above measures of social spending, governments sometimes shift the costs of their social policies to the private sector. For example:

* Federal law requires most hospitals with emergency departments to provide an “examination” and “stabilizing treatment” for anyone who comes to such a facility and requests care for an emergency medical condition or childbirth, regardless of their ability to pay and immigration status. This is mandated under a federal law called the Emergency Medical Treatment and Active Labor Act (EMTALA).[261] [262] [263] With regard to this law:

* Federal law give unions a monopoly over the labor supply of unionized bargaining units.[266] [267] In these workplaces:

* Federal law requires all nonprofit hospitals to treat Medicare and Medicaid patients.[270] During 2019:

* Since 2014, the Affordable Care Act (a.k.a. Obamacare) has required private health insurers to:

* The added costs of insuring people after they become ill raises the premiums of other customers.[276] [277] [278] [279] Per a 2016 report by Blue Cross Blue Shield (BCBS):

* The U.S. Constitution is the supreme legal authority in the United States. It is the written pact that established the U.S. government and vested it with certain powers. All presidents, governors, and federal/state judges and legislators are “bound by Oath or Affirmation, to support” it.[281] [282]

* Early during the convention at which the Constitution was written, Roger Sherman, a delegate from Connecticut and signatory to the Declaration of Independence, stated that the principal duties of a federal government should be to defend against foreign danger and internal uprisings, establish treaties, and regulate and tax trade with foreign nations.[283] [284]

* In response to Sherman, James Madison—who would later author the Bill of Rights and become known as the “Father of the Constitution” for his central role in its formation—stated that the items Sherman mentioned are all “important and necessary objects,” but they must be combined with “providing more effectually for the security of private rights and the steady dispensation of Justice.” He said that violations of these ideals “had more perhaps than any thing else, produced this convention.”[285] [286] [287]

* Continuing, Madison stated that all civilized societies are “divided into different sects, factions, and interests,” and “where a majority are united by a common interest or passion, the rights of the minority are in danger.” He then declared that:

* Towards that end, the framers of the Constitution developed a system of checks and balances on the powers of the government that they formed.[289] Guarding this system while giving it flexibility is Article V, which allows the Constitution to be amended with the approval of three-quarters of the states.[290] These provisions were designed to prevent a bare majority of people from oppressing all others.[291]

* In his farewell address to the nation, George Washington, the president of the Constitutional Convention and the first U.S. President,[292] [293] stated:

* After the Constitution was signed by the framers, it was submitted to the individual states for ratification. Written into the Constitution are the conditions that it would only be binding on the states that ratified it and would not become effective until at least nine of the states did so.[295] [296] During this ratification process, which lasted for three years,[297] there was opposition to the Constitution on several grounds, one of which was that it concentrated too much power in the hands of the federal government.[298] [299] [300]

* In an effort to build support for ratification of the Constitution,[301] three prominent statesmen collaborated in a series of essays known as the Federalist Papers, which explained the Constitution and addressed objections to it. These essays originally appeared in New York newspapers and were later assembled into book form and published throughout the states. The three authors were:

* Although the Federalist Papers were written by three individuals, all were signed with a single pen name: “Publius.” The book version of the Federalist Papers was edited by Alexander Hamilton, and the author’s name was given as “a Citizen of New York.”[303]

* Several of the objections voiced against the Constitution pertained to Article I, Section 8, which reads:

* One of the objections to this article was that the phrase, “provide for the common Defense and general Welfare,” gave the federal government broad powers to do whatever it felt was appropriate towards these ends.[305] In Federalist Paper 41, James Madison addressed this objection by stating that the phrase applied to and was limited by the specific powers detailed in the clauses that followed it (such as coining money, establishing federal courts, etc.). He said that to interpret the Constitution in any other way was “an absurdity.” He also wrote:

* In Federalist Paper 33, Alexander Hamilton addressed the objection that the last clause of Article 8, which grants the authority to make “all Laws” needed to carry out the powers vested in the Constitution, gave the federal government “comprehensive” power to tax citizens for a “vast number of” purposes.[307] In response, Hamilton wrote that the clause was “perfectly harmless” and only served to declare “a truth” that is a natural consequence of forming “a federal government and vesting it with certain specified powers.” He also wrote that it was an exaggeration to refer to this language as “sweeping,” and “if there is any thing exceptionable, it must be sought for in the specific powers upon which this general declaration is predicated.”[308]

* Between December 1787 and January 1791, the Constitution was ratified by all of the states.[309]

* Less than a year after the last state ratified the Constitution, Alexander Hamilton wrote a letter in which he asserted that the phrase “general Welfare” granted authority to the federal government beyond the specific powers detailed in Article 8. He said this phrase was “as comprehensive as any that could have been used” and it “embraces a vast variety of particulars, which are susceptible neither of specification nor of definition.”[310]

* Hamilton’s changed stance on federal power gave rise to a clash that led to the formation of the first two political parties in the United States: the Federalists led by Alexander Hamilton, and the Republicans led by James Madison and Thomas Jefferson, the primary author of the Declaration of Independence and third President of the United States. The Republicans later came to be called the “Democratic-Republicans,” and the modern Democratic Party traces their roots to this party and called Thomas Jefferson “the first Democratic President.”[311] [312] [313] [314] [315] [316] [317] [318]

* Conflict regarding the interpretation of the “general Welfare” clause spilled over into the 1800’s, during which it was a recurring issue whether or not the federal government had the authority to subsidize various projects on the grounds they promoted the general welfare. The name used for such activities was “internal improvements,” and this entailed items such as building roads and constructing canals on lands that were not federally owned.[319] [320]

* In 1817, James Madison, as President of the United States, vetoed an act “to set apart and pledge certain funds for internal improvements.” In doing so, he stated that the federal government did not have this power and to allow for it would require a distorted interpretation of the Constitution.[321] [322]

* When Madison vetoed this act, Thomas Jefferson wrote a letter praising this action and stating it was always “our tenet” that Congress does not have:

* In the same letter, Jefferson wrote he thought it was “fortunate” that Madison had the opportunity to veto such a bill because it:

* In 1824, John Quincy Adams was elected President of the United States. While in office, he proposed and signed various laws that appropriated federal funds for building roads, improving harbors, and subsidizing the arts and sciences.[326] [327] [328] While campaigning for President, he wrote the following to a voter who had asked about his view on internal improvements:

* In 1844, Democrat James Polk was elected President of the United States.[330] The argument was then being made that the following language in Article 8 of the Constitution gave the federal government authority to spend money on improving harbors and rivers:

* In a message to Congress, Polk responded that the phrase, “to regulate commerce” does:

* In 1848, the Democratic Party adopted a platform stating that the “federal government is one of limited powers” and:

* Three weeks after this platform was adopted, Abraham Lincoln, who was at the time a U.S. Congressman and a member of the Whig Party, gave a speech criticizing the Democratic Party’s stance on this issue. He briefly reviewed the opinions of past Presidents and jurists both pro and con, noted that the matter has not yet been brought under judicial consideration, and asserted there was no reason to worry about the constitutionality of such acts. He also stated:

* In 1856, Abraham Lincoln joined a new party that had been formed two years earlier on the basis of opposition to slavery.[336] [337] The name “Republican” was chosen for the party because the founders of it considered their principles to be aligned with that of Thomas Jefferson and the party he originally formed.[338] [339] The first Republican platform (1856) called for “restoring the action of the Federal Government to the principles of Washington and Jefferson.” It also stated that:

* In 1887, Congress passed a bill to supply seeds to drought-stricken farmers in Texas. Democratic President Grover Cleveland vetoed it, stating:

* In 1900, the Republican Party adopted a platform that voiced approval for “the improvement of the roads and highways,” but referred the matter to the states.[343]

* In 1900, the Democratic Party adopted a platform stating that the President and Congress derived their “existence” and “powers” from the Constitution and denounced the idea that they could “exercise lawful authority beyond it or in violation of it.” It also criticized a Republican-backed subsidy for the shipping industry and called for a “return to the time-honored Democratic policy of strict economy in governmental expenditures.”[344]

* In 1933, Franklin Delano Roosevelt, the Democratic governor of New York, became President of the United States.[345] The Great Depression had begun in 1929,[346] and upon accepting the nomination of the Democratic Party, Roosevelt promised a “new deal” for Americans. This entailed the elimination of nonessential government functions, an increase in government projects to stimulate employment, shortened working hours, and increased prices for agricultural goods to benefit the farming industry. In this acceptance speech, Roosevelt stated:

* As President, Roosevelt proposed a variety of bills to Congress. The House and Senate contained large Democratic majorities and passed most of Roosevelt’s proposals.[349] [350] [351] This included, among other measures:

* Much of this legislation was challenged in court, and between January 1935 and May 1936, the Supreme Court ruled on ten such major cases. In eight of these, the laws were struck down in part or whole for overstepping the bounds of power granted to the federal government in the Constitution.[361] Four of the nine justices generally ruled against the New Deal programs, three generally ruled in favor of them, and two of the justices were swing votes.[362]

* In Carter v. Carter Coal Company, the Supreme Court (voting 6–3) struck down a federal law that placed taxes on coal, fixed coal prices, paid money to coal producers who agreed to follow federal edicts, and established provisions for industry-wide wage requirements.[363] The majority ruling stated that the Constitutional Convention:

* In Schechter Poultry Corporation v. United States, the Supreme Court unanimously struck down a law that gave the President the power to enact separate “codes of fair competition” for wide-ranging industries and trades. This included the authority to fix the prices of goods and services, set minimum wages, set maximum working hours, and at the discretion of the President, revoke the business license of anyone he judged to be incompliant with these codes.[365] [366] [367]

* In Schechter, seven of the nine justices joined in the majority ruling, and the two remaining justices concurred with differing language. In this decision, the majority cited the Tenth Amendment, which affirms that any powers not granted to the federal government by the Constitution belong to the States or to the people. The ruling stated:

* Four days after this decision was issued, Roosevelt held a press conference in which he asserted that the “implications of this decision are much more important than certainly any decision of my lifetime or yours,” and that the Supreme Court had “relegated” the U.S. to a “horse and buggy” interpretation of the Constitution. When a reporter asked him if there was any suggestion as to how to resolve the matter outside of a Constitutional Amendment, Roosevelt replied, “No; we haven’t gotten to that yet.”[369]

* Four months before this press conference, Roosevelt’s Secretary of the Interior, Harold L. Ickes, recorded the following in his diary:

* The following year, Roosevelt won reelection by a broad margin, and the Democratic Party expanded its majorities in the House and Senate. [371] [372] After his term began, Roosevelt proposed a bill that would have granted him provisions to appoint up to six more justices to the Supreme Court.[373] [374] [375] At the press conference in which he announced this proposal, he stated:

* Seven years before this, as the governor of New York, Roosevelt stated:

* In the four months after Roosevelt proposed his bill to alter the composition of the Supreme Court,[378] the Court ruled in six cases concerning New Deal legislation. In all of these decisions, the Court voted to uphold the acts under consideration. Five of these cases were decided by a 5 to 4 margin, with the two swing justices casting the determinative votes.[379] [380] [381] [382] [383] [384] [385]

* In Steward Machine Company v. Davis, the Supreme Court (voting 5–4) upheld a federal law imposing new taxes that were ultimately given to unemployed people.[386] [387] In this decision, the majority cited unemployment statistics and stated:

* The two swing justices, Charles Evan Hughes and Owen J. Roberts joined in this decision.[388] [389]

* One year earlier, Justice Roberts joined in a decision that stated the Constitution:

* One year before this, Justice Roberts joined in a decision written by Justice Hughes that stated:

* In the same month that the last of these decisions was issued, one of the justices who generally ruled against the New Deal programs announced his retirement. The next month, Roosevelt’s bill to add justices to the Supreme Court was defeated in the Senate Judiciary Committee by a vote of 10 to 8.[392] [393] Seven of the ten Senators voting against this bill were Democrats.[394]

* Over the next two years, all of the justices that generally found the New Deal programs to be unconstitutional either retired or passed on.[395] In 1938, Roosevelt stated:

* By 1944, seven of the nine justices on the Supreme Court had been appointed by Roosevelt.[397] Over the next half century, the Supreme Court did not rule any major social spending program to be unconstitutional.[398]

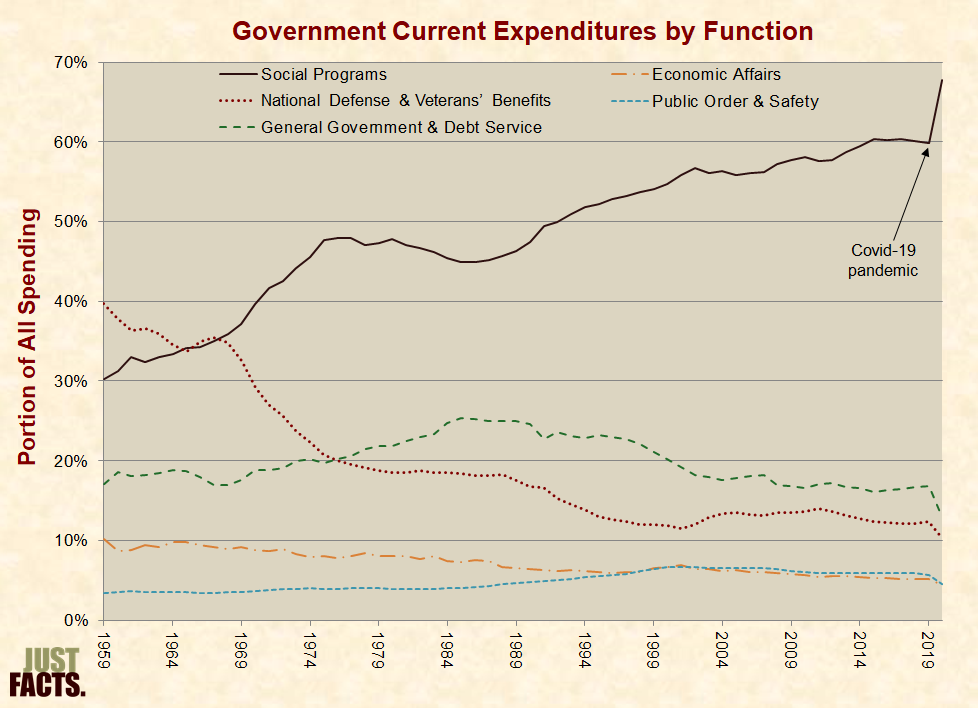

* In 2020, the federal government spent 73% of its finances on social programs, including income security, healthcare, education, housing, and recreation. This amounts to $5.0 trillion or an average of $38,662 for every household in the U.S.[399]

* From 1959 to 2020, the portion of federal outlays that were spent on:

* A scientific, nationally representative survey commissioned in 2020 by Just Facts found that 50% of voters believe social spending is not the main cause of rising national debt.[404] [405] [406]

[1] Article: “Social Welfare Program.” Encyclopædia Britannica. Accessed May 11, 2018 at <www.britannica.com>

“Social welfare program, any of a variety of governmental programs designed to protect citizens from the economic risks and insecurities of life. The most common types of programs provide benefits to the elderly or retired, the sick or invalid, dependent survivors, mothers, the unemployed, the work-injured, and families.”

[2] Report: “Social Welfare Expenditures Under Public Programs, Fiscal Year 1977.” By Alma McMillan. Social Security Administration, Office of Research and Statistics Social Security Bulletin, June 1979. <www.ssa.gov>

Page 7:

Public social welfare expenditures are defined in this series as cash and medical benefits, services, and administrative costs for all programs operating under public law that are of direct benefit to individuals and families. Included are programs providing income maintenance and health benefits through social insurance and public aid, and those providing public support of health, education, housing, and other welfare services.

[3] Article: “Social Welfare Expenditures in the United States, 1956–57.” By Ida C. Merriam (Director, Division of Program Research, Office of the Social Security Commissioner). Social Security Bulletin, October 1958. Pages 22–33. <www.ssa.gov>

Page 22:

Whatever definition of social welfare programs or activities is used, there are several different contexts in which it is desirable to look at social welfare expenditures. The primary one around which the series has been organized is that of program expenditures. This classification identifies total expenditures, including costs of administration, under designated programs—in this instance, civilian public programs of income maintenance, health, education, public housing, and other welfare services. The data thus compiled give a measure of the shares of the total national output and of all public expenditures that have been going to these designated programs.

[4] The Oxford Handbook of U.S. Social Policy. Edited by Daniel Beland, Christopher Howard, and Kimberly J. Morgan. Oxford University Press, 2015.

Chapter 1: “The Fragmented American Welfare State: Putting the Pieces Together.” By Daniel Beland, Christopher Howard, and Kimberly J. Morgan. Pages 3–22.

Page 4:

Social policy refers to programs that redistribute resources across society and often seek to cushion people against life’s socioeconomic risks. These programs usually take the form of cash transfers or in-kind benefits such as medical care. Taken together, social programs constitute the welfare state, a term that implies uniformity and coherence but in fact often conceals a tremendous amount of variation in terms of programmatic design and political dynamics.

… Modern social programs span a multitude of policy areas, including programs for the unemployed, retirees, the sick, the disabled, the poor, and families with children (Beland 2010). All of these policy areas are explicitly analyzed in this handbook. Some, such as retirement pensions and health care, are represented by several chapters each, a reflection of the programmatic complexity and fragmentation of the American welfare state.

[5] Working paper: “Is the European Welfare State Really More Expensive? Indicators on Social Spending, 1980–2012; and a Manual to the OECD Social Expenditure Database (SOCX).” By Willem Adema, Pauline Fron, and Maxime Ladaique. Organization for Economic Cooperation and Development, 2011. <www.oecd-ilibrary.org>

Page 90:

II.2. Defining the Social Domain

68. To facilitate cross-country comparisons of social expenditure, the first step is to demarcate what spending is ‘social’ and what is not. The OECD [Organization for Economic Cooperation and Development] defines social expenditures as: “The provision by public and private institutions of benefits to, and financial contributions targeted at, households and individuals in order to provide support during circumstances which adversely affect their welfare, provided that the provision of the benefits and financial contributions constitutes neither a direct payment for a particular good or service nor an individual contract or transfer.”

69. Since only benefits provided by institutions are included in the social expenditure definition, transfers between households—albeit of a social nature, are not in the social domain.10

70. Social benefits include cash benefits (e.g., pensions, income support during maternity leave and social assistance payments), social services (e.g., childcare, care for the elderly and disabled) and tax breaks with a social purpose (e.g., tax expenditures towards families with children, or favourable tax treatment of contributions to private health plans).

71. There are two main criteria which have to be simultaneously satisfied for an expenditure item to be classified as social. First, the benefits have to be intended to address one or more social purposes. Second, programmes regulating the provision of benefits have to involve either a) inter-personal redistribution, or b) compulsory participation.

II.2.1. Towards a Social Purpose

72. The OECD Social Expenditure Database groups benefits with a social purpose in nine policy areas (see also section II.3.1 for more detail):

• Old-age – pensions (see Box II.2), early retirement pensions, home-help and residential services for the elderly;

• Survivors – pensions and funeral payments;

• Incapacity-related benefits – care services, disability benefits, benefits accruing from occupational injury and accident legislation, employee sickness payments;

• Health – spending on in- and out-patient care, medical goods, prevention;

• Family – child allowances and credits, childcare support, income support during leave, sole parent payments;

• Active labour market policies – employment services, training, employment incentives integration of the disabled, direct job creation, and start-up incentives;

• Unemployment – unemployment compensation, early retirement for labour market reasons;

• Housing – housing allowances and rent subsidies; and,

• Other social policy areas – non-categorical cash benefits to low-income households, other social services; i.e., support programmes such as food subsidies, which are prevalent in some non-OECD countries.

10 Social spending does not include remuneration for work, as it does not cover market transactions, i.e., payments in return for the simultaneous provision of services of equivalent value. Employer costs such as allowances towards transport, holiday pay, etc. are part of remuneration in this sense.

[6] Appendix: “Estimating Public Social Expenditure 2014/15–2016, Sources and Methods.” Organization for Economic Cooperation and Development, October 12, 2016. <www.oecd.org>

Page 3:

Social transfers in kind consist of individual goods and services provided as transfers in kind to individual households by government units. They include:

Social benefits in kind (D.631). Social benefits in kind are social transfers in kind intended to relieve the household from the financial burden of social risks or needs. They include the following cases:

• Social security benefits, reimbursements (D.6311). These benefits consist of reimbursement by social security funds of approved expenditures made by households on specific goods or services.

• Other social security benefits in kind (D.6312). These consist of transfers in kind provided to households by government units that are similar in nature to social security benefits in kind but are not provided in the context of social insurance schemes. Social assistance benefits in kind include, if not covered by a social insurance scheme, for instance social housing, dwelling allowances, and reduction of transport prices (provided that there is a social purpose).

Transfers of individual non-market goods or services (D.632). Transfers of individual non-market goods or services consist of goods or services provided to individual households free or at prices which are not economically significant, by non-market producers of government units. They cover for instance education and cultural services.

[7] Article: “Social Welfare Expenditures, 1929–67.” By Ida C. Merriam (Assistant Commissioner, Office of Research and Statistics, Social Security Administration). Social Security Bulletin, December 1967. Pages 3–16. <www.ssa.gov>

Page 3:

The long-time upward trend in social welfare expenditures, both in absolute amounts and as a percent of the gross national product, continued in the fiscal year 1967. So did the increasing importance of the Federal sector. Total social welfare expenditures for the first time passed the $100 billion mark and amounted to 13 percent of the gross national product ($763 billion). Federal funds accounted for 54 percent of all social welfare expenditures. The largest single increase was the $3.3 billion for health insurance for the aged under the Social Security Act (Medicare).

Just before the turn of the century, total social welfare expenditures amounted to about 2.4 percent of the gross national product with expenditures for education—almost entirely from State and local funds—making up almost half the total. Veterans’ benefits, more than one third of the total, were the only significant Federal social welfare expenditures. The great depression of the 1930’s brought the Federal Government into the area of social welfare activities in a major way. Significant growth in the population and in the number of risks covered by social insurance, as well as an accelerating Federal involvement in health and education programs, has been largely responsible for the rising trends in social welfare expenditures since the late 1950’s. The increasing number of children and older persons in the population, accompanied by the prolonging of school years and a trend toward early retirement have had their effect on both transfer payments and service programs.

Pages 5–6:

Ten years from today programs now omitted from the social welfare series may appear to be obviously an aspect of social welfare policy that should be included. For the present, the general boundary line of programs designed specifically to deal with individual welfare has been retained, and the series continues to exclude such community services as urban transportation, city planning and urban renewal, water and sewer works, preservation of law and order, and parks and recreation. Admittedly, the dividing line is arbitrary. Some legal aid services are included with the special OEO [Office of Economic Opportunity] programs and some juvenile delinquency services with child welfare. But the maintenance of courts, police departments, reform schools, and prisons seem better treated as a general function of government and omitted from this series. Similarly, one can recognize the importance of urban transportation in assuring access to jobs and steady earnings without classifying it as a social welfare program. Recreational facilities, or at least organized recreational services, and library services may be regarded as closer to the borderline. They continue to be omitted, however, except where they may be hidden in expenditures for schools or other activities. Unless such distinctions were retained, the series would become almost a listing of government expenditures for nondefense purposes and lose much of its intended character and usefulness.

The series continues to relate to direct expenditures and to exclude such indirect types of subsidy or support as loans, loan guarantees, or income-tax exemptions. The basic series relates to public programs. Related private expenditures for health, education, and income maintenance and welfare services are brought together in the regular Bulletin series, as heretofore.

Table l.—Social Welfare Expenditures Under Public Programs, Selected Fiscal Years, 1928–29 Through 1966–67 …

Social insurance

Old-age, survivors, and disability insurance [Social Security]

Health insurance for the aged [Medicare]

Railroad retirement

Public employee retirement

Unemployment insurance and employment service

Railroad unemployment insurance

Railroad temporary disability insurance

State temporary disability insurance

Hospital and medical benefits

Workmen’s compensation

Hospital and medical benefits

Public aid

Public assistance

Vendor medical payments

Other

Health and medical programs

Hospital and medical care

Civilian programs

Defense Department

Maternal and child health programs

Medical research

School health (educational agencies)

Other public health activities

Medical-facilities construction

Defense Department

Other

Veterans’ programs

Pensions and compensation

Health and medical programs

Hospital and medical care

Hospital construction

Medical and prosthetic research

Education

Life insurance

Welfare and other

Education

Elementary and secondary

Construction

Higher

Construction

Vocational and adult

Housing

Public housing

Other

Other social welfare

Vocational rehabilitation

Medical services

Medical research

Institutional care

School meals

Child welfare

Special OEO programs

Social welfare, not elsewhere classified

[8] Book: Early Childhood Care and Education in Canada: Past, Present, and Future. Edited by Larry Prochner and Nina Howe. UBC Press, 2000.

Chapter 9: “Child Care as a Social Policy Issue.” By Martha Friendly. Pages 252–273.

Page 261:

In the twentieth century, Canadian approaches to social programs have been characterized by two main shifts in perception and treatment. In the nineteenth century, health and education were considered to be private responsibilities; and at the time of Confederation, social welfare had not yet developed as an issue. When there was a need for social assistance outside the nuclear and extended family, it generally fell within the domain of churches; later, non-religious charitable institutions assumed responsibility for assisting the deserving poor and needy. A good example of an early foray into what had previously been in the private realm were mothers’ pensions, originally introduced to provide support to needy mothers of young children who were “deserving” because they had been widowed in the First World War (Guest 1990).

The first conceptual shift was that from the original individualistic, family-centred or, at most, charitable view to one of increased collective responsibility. This first shift occurred between the end of the Second World War and the early 1970s, when Canada’s main social programs—health care, unemployment insurance, pensions, and social welfare—were emerging. Over this period, governments, both federal and provincial, assumed a major responsibility for these functions, with the federal government assuming a policy-shaping role, and the provinces becoming the program managers and deliverers (Doherty, Friendly, and Oloman 1998).

Most of Canada’s health, educational and social programs were developed as universal or inclusive programs (sometimes called “institutional”). National health care, or medicare, is perhaps the best example of the way a social policy has defined its target group as all Canadians, rather than the poor or needy; postsecondary, elementary and secondary education, Unemployment Insurance, and Canada Pension were also developed as universal programs.

[9] Book: Aging and Social Expenditure in the Major Industrial Countries, 1980–2025. By Peter S. Heller, Richard Hemming, Peter Kohnert, and a staff team from the Fiscal Affairs Department. International Monetary Fund, 1986.

Page 1: “The focus is on government expenditure in the different social sectors. Social expenditure is defined to include, as a central core, medical care, education, pensions, welfare payments, unemployment insurance, and family benefits. A smaller residual category of social expenditure is included which differs across countries (see Chapter 11).”

Page 16:

An important problem faced in undertaking this study, particularly given its cross-country focus, was how to define the social expenditure of the government. Clearly, one should include expenditure on education, medical care, pensions, unemployment compensation, and income maintenance for the poor. The dividing line then becomes blurred. Should one include expenditure on family allowances? veterans benefits? workmen’s compensation? Should pensions of central government or public enterprise employees be included or treated analogously to with private sector employees?

[10] Calculated with data from:

a) Report: “Annual Statistical Supplement to the Social Security Bulletin, 2002.” Social Security Administration, February 25, 2003. <www.ssa.gov>

Page 130: “Table 3.A1—Gross domestic product (GDP) and social welfare expenditures under public programs, selected fiscal years 1965–1995 … Amount (millions of dollars) … Total social welfare expenditures b … 1995 [=] 1,505,136”

b) Dataset: “Table 3.1. Government Current Receipts and Expenditures [Billions of Dollars] Seasonally Adjusted at Annual Rates.” U.S. Bureau of Economic Analysis. Last revised May 26, 2022. <apps.bea.gov>

“Total expenditures … 1994 … Q4 [=] 2,544.7 … 1995 … Q1 [=] 2,582.4 … Q2 [=] 2,610.5 … Q3 [=] 2,598.8”

c) United States Code Title 31, Subtitle II, Chapter 11, Section 1102: “Fiscal Year.” Accessed June 21, 2022 at <www.law.cornell.edu>

“The fiscal year of the Treasury begins on October 1 of each year and ends on September 30 of the following year.”

CALCULATION: $1,505,136 million social welfare expenditures / (($2,544.7 + $2,582.4 + $2,610.5 + $2,598.8) /4) billion government spending = 58%

[11] Report: “Fiscal Year 2023 Historical Tables: Budget Of The U.S. Government.” White House Office of Management and Budget, March 2022. <www.whitehouse.gov>

“Table 3.1—Outlays by Superfunction and Function: 1940–2027.” (<www.whitehouse.gov>)

“In millions of dollars … Human resources … 2021 [=] 4,807,912 … As percentages of outlays … Human resources … 2021 [=] 70.5%”

NOTE: Credit for bringing this measure to the attention of Just Facts belongs to Jodie Carroll of Vote Facts (<www.votefacts.org>).

[12] Calculated with data from:

a) Dataset: “Table 3.16. Government Current Expenditures by Function [Billions of Dollars].” U.S. Bureau of Economic Analysis. Last revised October 29, 2021. <apps.bea.gov>

b) Report: “Fiscal Year 2023 Historical Tables: Budget Of The U.S. Government.” White House Office of Management and Budget, March 2022. <www.whitehouse.gov>

“Table 3.1—Outlays by Superfunction and Function: 1940–2027.” (<www.whitehouse.gov>)

NOTES:

[13] Calculated with data from:

a) Dataset: “Table 3.12. Government Social Benefits [Billions of Dollars].” U.S. Bureau of Economic Analysis. Last revised July 30, 2021. <apps.bea.gov>

b) “2018 Actuarial Report on the Financial Outlook for Medicaid.” By Christopher J. Truffer and others. U.S. Department of Health & Human Services, Centers for Medicare and Medicaid Services, Office of the Actuary, 2019. <www.cms.gov>

Page 3: “Medicaid costs are met primarily by Federal and State general revenues, on an as-needed basis; the States may also rely on local government revenues to finance a portion of their share of Medicaid costs.”

c) Email from the U.S. Bureau of Economic Analysis to Just Facts, September 7, 2018.

“The reason we don’t classify them [federal Medicaid outlays] as [federal] ‘Government Social Benefits’ is because the [federal] government doesn’t make these payments directly to individuals, but rather sends money to the states and the states distribute the benefits.”

d) Dataset: “National Health Expenditures by Type of Service and Source of Funds, Calendar Years 1960–2020.” U.S. Department of Health & Human Services, Centers for Medicare and Medicaid Services, December 1, 2021. <www.cms.gov>

e) Dataset: “Table 3.1. Government Current Receipts and Expenditures [Billions of Dollars] Seasonally Adjusted at Annual Rates.” U.S. Bureau of Economic Analysis. Last revised May 26, 2022. <apps.bea.gov>

f) Dataset: “Table 3.2. Federal Government Current Receipts and Expenditures.” U.S. Bureau of Economic Analysis. Last revised May 26, 2022. <apps.bea.gov>

NOTE: An Excel file containing the data and calculations is available upon request.

[14] Full documentation for each of the measures is provided in these sections below:

Social Welfare Expenditures is not included in this chart, because complete historical data for this measure is unavailable.

[15] Calculated with data from:

a) Report: “CBO Estimate for H.R. 6074, the Coronavirus Preparedness and Response Supplemental Appropriations Act, 2020, as Posted on March 4, 2020.” Congressional Budget Office, March 4, 2020. <www.cbo.gov>

b) Report: “Cost Estimate for H.R. 6201, Families First Coronavirus Response Act, Enacted as Public Law 116-127 on March 18, 2020.” Congressional Budget Office, April 2, 2020. <www.cbo.gov>

c) Report: “Cost Estimate for H.R. 748, CARES Act, Public Law 116-136.” Congressional Budget Office, April 16, 2020. <www.cbo.gov>

d) Report: “CBO Estimate for H.R. 266, the Paycheck Protection Program and Health Care Enhancement Act as Passed by the Senate on April 21, 2020.” Congressional Budget Office, April 22, 2020. <www.cbo.gov>

e) Report: “Estimate for Division N—Additional Coronavirus Response and Relief, H.R. 133, Consolidated Appropriations Act, 2021, Public Law 116-260, Enacted on December 27, 2020.” Congressional Budget Office, January 14, 2021. <www.cbo.gov>

f) Report: “Estimated Budgetary Effects of H.R. 1319, American Rescue Plan Act of 2021 as Passed by the Senate on March 6, 2021.” Congressional Budget Office, March 10, 2021. <www.cbo.gov>

g) Dataset: “HH-1. Households by Type: 1940 to Present.” U.S. Census Bureau, Current Population Survey, November 2021. <www.census.gov>

NOTE: An Excel file containing the data and calculations is available upon request.

[16] Report: “Social Welfare Expenditures Under Public Programs, Fiscal Year 1977.” By Alma McMillan. Social Security Administration, Office of Research and Statistics Social Security Bulletin, June 1979. <www.ssa.gov>

Page 7:

Public social welfare expenditures are defined in this series as cash and medical benefits, services, and administrative costs for all programs operating under public law that are of direct benefit to individuals and families. Included are programs providing income maintenance and health benefits through social insurance and public aid, and those providing public support of health, education, housing, and other welfare services.

[17] Report: “Annual Statistical Supplement to the Social Security Bulletin, 2002.” Social Security Administration, February 25, 2003. <www.ssa.gov>

Page 130:

Total social welfare expenditures b …

b Represents program and administrative expenditures from federal, state and local public revenues and trust funds under public law. Includes workers’ compensation and temporary disability insurance payments made through private carriers and self-insurers. Includes capital outlay and some expenditures abroad.

NOTES:

[18] Article: “Great Depression.” By Richard H. Pells and Christina D. Romer. Encyclopedia Britannica, 1998. <www.britannica.com>

“Great Depression, worldwide economic downturn that began in 1929 and lasted until about 1939. It was the longest and most severe depression ever experienced by the industrialized Western world, sparking fundamental changes in economic institutions, macroeconomic policy, and economic theory.”

[19] Article: “Roosevelt, Franklin Delano.” By James T. Patterson (Ph.D., Professor of History, Brown University). World Book Encyclopedia, 2007 Deluxe Edition.

“Roosevelt became president on March 4, 1933, at the age of 51. The inauguration was the last held in March. Under Amendment 20 to the Constitution, all later inaugurations have been held in January.”

[20] Article: “Roosevelt, Franklin Delano.” By James T. Patterson (Ph.D., Professor of History, Brown University). World Book Encyclopedia, 2007 Deluxe Edition.

“On March 9, 1933, Congress began a special session called by Roosevelt. The president at once began to submit recovery and reform laws for congressional approval. Congress passed nearly all the important bills that he requested, most of them by large majorities.”

[21] Table constructed with data from:

a) Webpage: “Party Divisions of the House of Representatives.” Office of the Clerk, United States House of Representatives. Accessed October 25, 2018 at <history.house.gov>

b) Webpage: “Party Division in the Senate, 1789–Present.” Historical Office, United States Senate. Accessed October 25, 2018 at

|

Election Year |

Congress |

House of Representatives |

Senate |

||

|

Democrats |

Republicans |

Democrats |

Republicans |

||

|

1930 |

72nd (1931–33) |

216 |

218 |

47 |

48 |

|

1932 |

73rd (1933–35) |

313 |

117 |

59 |

36 |

|

1934 |

74th (1935–37) |

322 |

103 |

69 |

25 |

|

1936 |

75th (1937–39) |

334 |

88 |

76 |

16 |

|

1938 |

76th (1939–41) |

262 |

169 |

69 |

23 |

|

1940 |

77th (1941–43) |

267 |

162 |

66 |

28 |

[22] Book: The American Constitution: Its Origins and Development (3rd edition). By Alfred H. Kelly and Winfred A. Harbison. W. W. Norton & Company, 1963.

Page 792: “Franklin D. Roosevelt’s administration was the first one to assume that it was the federal government’s duty to assume responsibility for virtually all the important phases of the entire national economy—production, labor, unemployment, social security, money and banking, housing, public works, flood control, and the conservation of natural resources.”

[23] Article: “New Deal.” By David A. Shannon (Ph.D., Former Professor of History, University of Virginia). World Book Encyclopedia, 2007 Deluxe Edition.

“The Federal Emergency Relief Administration provided the states with money for the needy.”

[24] Article: “New Deal.” By David A. Shannon (Ph.D., Former Professor of History, University of Virginia). World Book Encyclopedia, 2007 Deluxe Edition.

“The United States Housing Act of 1937 ‘provided money for more federal public housing projects.’ ”

[25] “The Social Security Act of 1935.” United States Congress, August 14, 1935. <www.ssa.gov>

An act to provide for the general welfare by establishing a system of Federal old-age benefits, and by enabling the several States to make more adequate provision for aged persons, blind persons, dependent and crippled children, maternal and child welfare, public health, and the administration of their unemployment compensation laws; to establish a Social Security Board; to raise revenue; and for other purposes.

[26] Article: “Roosevelt, Franklin D.” Encyclopædia Britannica Ultimate Reference Suite 2004.

“The Home Owners’ Refinancing Act provided mortgage relief for millions of unemployed Americans in danger of losing their homes.”

[27] Article: “New Deal.” By David A. Shannon (Ph.D., Former Professor of History, University of Virginia). World Book Encyclopedia, 2007 Deluxe Edition.

“The Home Owners Loan Corporation (HOLC) provided money at low interest for persons struggling to pay mortgages.”

[28] Article: “Federal Reserve’s Role During WWII.” By Gary Richardson. Federal Reserve Bank of Richmond, Federal Reserve History, November 22, 2013. <www.federalreservehistory.org>

In September 1939, Germany’s invasion of Poland triggered war among the principal European powers. In December 1941, Japan attacked Pearl Harbor. Germany and Italy declared war on the United States. The American “arsenal of democracy” joined the Allied nations, including Britain, France, China, the Soviet Union, and numerous others, in the fight against the Axis alliance. The Allied counteroffensive began in 1942. The Axis surrendered in 1945.

[29] Article: “World War II.” Encyclopædia Britannica Ultimate Reference Suite 2004.

[It was] also called Second World War, a conflict that involved virtually every part of the world during the years 1939–45. The principal belligerents were the Axis powers—Germany, Italy, and Japan—and the Allies—France, Great Britain, the United States, the Soviet Union, and, to a lesser extent, China. The war was in many respects a continuation, after an uneasy 20-year hiatus, of the disputes left unsettled by World War I. The 40,000,000–50,000,000 deaths incurred in World War II make it the bloodiest conflict as well as the largest war in history.

[30] Article: “Great Society.” Encyclopædia Britannica Ultimate Reference Suite 2004.

[A] political slogan used by U.S. President Lyndon B. Johnson (served 1963–69) to identify his legislative program of national reform. … He called for an enormous program of social welfare legislation including federal support for education, medical care for the aged through an expanded Social Security Program, and federal legal protection for citizens deprived of the franchise by certain state registration laws. After a landslide victory for the Democratic Party in the elections of November 1964, a sympathetic Congress passed almost all the president’s bills.

[31] Video: “State of Union Address.” By Lyndon B. Johnson, January 8, 1964. <www.youtube.com>

Time marker 3:00:

Let this session of Congress be known as the session which …

• enacted the most far-reaching tax cut of our time. …

• declared all-out war on human poverty and unemployment in these United States. …

• helped to build more homes and more schools and more libraries and more hospitals than any single session of Congress in the history of our Republic. …

All this and more can and must be done. It can be done by this summer, and it can be done without any increase in spending. In fact, under the budget that I shall shortly submit, it can be done with an actual reduction in federal expenditures and federal employment.

Time marker 12:45:

This budget and this year’s legislative program are designed to help each and every American citizen fulfill his basic hopes. His hope for a fair chance to make good, his hope for fair play from the law, his hope for a full-time job on full-time pay, his hopes for a decent home for his family in a decent community, his hopes for a good school for his children with good teachers, and his hopes for security when faced with sickness, or unemployment, or old age.

Unfortunately, many Americans no longer have hope, some because of their poverty, and some because of their color, and all too many because of both. Our task is to help replace their despair with opportunity, and this administration today here and now declares unconditional war on poverty in America.

Time marker 14:17: “And I urge this Congress and all Americans to join with me in that effort. It will not be a short or easy struggle. No single weapon or strategy will suffice, but we shall not rest until that war is won.”

Time marker 15:30: “Poverty is a national problem requiring improved national organization and support. For this attack to be effective, it must also be organized at the state and the local level and must be supported and directed by state and local efforts.”

Time marker 18:10:

Our aim is not only to relieve the symptom of poverty but to cure it, and above all, to prevent it.

No single piece of legislation, however, is going to suffice. We will launch a special effort in the chronically distressed areas of Appalachia. We must expand our small but our successful area redevelopment program.

We must enact youth employment legislation to put jobless, aimless, hopeless youngsters to work on useful projects.

We must distribute more food to the needy through a broader Food Stamp program. We must create a national service corps to help the economically handicapped of our own country as the Peace Corps now helps those abroad.

We must modernize our unemployment insurance and establish a high-level commission on automation. If we have the brainpower to invent these machines, we have the brainpower to make certain that they are a boon and not a bane to humanity.

We must extend the coverage of our minimum wage laws to more than two million workers now lacking this basic protection of purchasing power.

We must, by including special school aid funds as part of our education program, improve the quality of teaching, and training, and counseling in our hardest hit areas.

We must build more libraries in every area, and more hospitals and nursing homes under the Hill-Burton Act, and train more nurses to staff them.

We must provide hospital insurance for older citizens financed by every worker and his employer under Social Security, contributing no more than $1 a month during the employee’s working career to protect him in his old age in a dignified manner without cost to the Treasury against the devastating hardship of prolonged or repeated illness.

We must, as a part of a revised housing and urban renewal program, give more help to those displaced by slum clearance, provide more housing for our poor and our elderly, and seek as our ultimate goal in our free enterprise system, a decent home for every American family.

We must help obtain more modern mass transit within our communities, as well as low-cost transportation between them.

Above all, we must release $11 billion of tax reduction into the private spending stream to create new jobs and new markets in every area of this land.

[32] Calculated with data from:

a) Book: Historical Statistics of the United States, Colonial Times to 1970 (Part 1). U.S. Census Bureau, September 1975. <fraser.stlouisfed.org>

Page 340: “Series H 1-31. Social Welfare Expenditures Under Public Programs: 1890 to 1970 [In millions of dollars. Years ending June 30 for Federal Government, most States, and some localities]”

b) Report: “Annual Statistical Supplement to the Social Security Bulletin, 2002.” Social Security Administration, February 25, 2003. <www.ssa.gov>

Page 130: “Table 3.A1—Gross domestic product (GDP) and social welfare expenditures under public programs, selected fiscal years 1965–1995”

c) Dataset: “Nominal GDP (Millions of Dollars), 1790–2017.” By Louis Johnston and Samuel H. Williamson. MeasuringWorth. Accessed October 30, 2018 at <www.measuringworth.com>

NOTE: An Excel file containing the data and calculations is available upon request.

[33] Report: “Fiscal Year 2023 Historical Tables: Budget of the U.S. Government.” White House Office of Management and Budget, March 2022. <www.whitehouse.gov>

Table 3.1—Outlays by Superfunction and Function: 1940–2027 (<www.whitehouse.gov>)

Human resources

Education, Training, Employment, and Social Services

Health

Medicare

Income Security

Social Security …

Veterans Benefits and Services

Table 3.2—Outlays by Function and Subfunction: 1940–2027 (<www.whitehouse.gov>)

500 Education, Training, Employment, and Social Services:

501 Elementary, secondary, and vocational education

502 Higher education

503 Research and general education aids

504 Training and employment

505 Other labor services

506 Social services …

550 Health:

551 Health care services

552 Health research and training

554 Consumer and occupational health and safety …

570 Medicare …

600 Income Security:

601 General retirement and disability insurance (excluding social security)

602 Federal employee retirement and disability

603 Unemployment compensation

604 Housing assistance

605 Food and nutrition assistance

609 Other income security …

650 Social Security [officially, Old-Age, Survivors, and Disability Insurance] …

700 Veterans Benefits and Services:

701 Income security for veterans

702 Veterans education, training, and rehabilitation

703 Hospital and medical care for veterans

704 Veterans housing

705 Other veterans benefits and services

NOTE: Credit for bringing this measure to the attention of Just Facts belongs to Jodie Carroll of Vote Facts (<www.votefacts.org>).

[34] Report: “Analytical Perspectives: Budget of the U.S. Government, Fiscal Year 2023.” White House Office of Management and Budget, April 2022. <www.whitehouse.gov>

Page 104: “The budget records refunds of receipts that result from overpayments by the public (such as income taxes withheld in excess of tax liabilities) as reductions of receipts, rather than as outlays. However, the budget records payments to taxpayers for refundable tax credits (such as earned income tax credits) that exceed the taxpayer’s tax liability as outlays.”

[35] Report: “Overview of the Federal Tax System in 2022.” By Molly F. Sherlock and Donald J. Marples. Congressional Research Service. Updated June 8, 2022. <sgp.fas.org>

Page 8: “If a tax credit is refundable, and the credit amount exceeds tax liability, a taxpayer receives the credit (or a portion of the credit) as a refund. … Some [tax] credits are phased out as income rises to limit or eliminate benefits for higher-income taxpayers.”

[36] Report: “Fiscal Year 2023 Historical Tables: Budget of the U.S. Government.” White House Office of Management and Budget, March 2022. <www.whitehouse.gov>

Table 3.1—Outlays by Superfunction and Function: 1940–2027 (<www.whitehouse.gov>)

Human resources …

Income Security

Table 3.2—Outlays by Function and Subfunction: 1940–2027 (<www.whitehouse.gov>)

600 Income Security:

601 General retirement and disability insurance (excluding social security)

602 Federal employee retirement and disability

603 Unemployment compensation

604 Housing assistance

605 Food and nutrition assistance

609 Other income security

NOTE: Credit for bringing this measure to the attention of Just Facts belongs to Jodie Carroll of Vote Facts (<www.votefacts.org>).

[37] Report: “Analytical Perspectives: Budget of the U.S. Government, Fiscal Year 2023.” White House Office of Management and Budget, April 1, 2022. <www.whitehouse.gov>

Supplement: “Table 22-12: Baseline Net Outlays by Function, Category, and Program.” White House Office of Management and Budget, March 2022. <www.whitehouse.gov>

Page 20 (of PDF):

600 Income Security: …

609 Other income security: …

U.S. Coronavirus Payments

[38] Report: “Analytical Perspectives: Budget of the U.S. Government, Fiscal Year 2023.” White House Office of Management and Budget, April 1, 2022. <www.whitehouse.gov>

Page 44:

Net financing disbursements of the direct loan and guaranteed loan financing accounts.—Under the Federal Credit Reform Act of 1990 (FCRA),9 the budgetary program account for each credit program records the estimated subsidy costs—the present value of estimated net losses—at the time when the direct or guaranteed loans are disbursed. The individual cash flows to and from the public associated with the loans or guarantees, such as the disbursement and repayment of loans, the default payments on loan guarantees, the collection of interest and fees, and so forth, are recorded in the credit program’s non-budgetary financing account.

Page 257:

SBA [U.S. Small Business Administration] supported American communities that needed access to low-interest loans to recover quickly in the wake of disaster, especially due to the COVID-19 pandemic. By the end of 2021, the SBA had made approximately $320 billion in COVID Economic Injury Disaster Loans, providing low-interest working capital to small businesses across the country to help address the negative economic impacts of the pandemic. To further assist with COVID-19 relief, Congress created the Paycheck Protection Program (PPP) under the CARES Act [Coronavirus Aid, Relief, and Economic Security Act] to provide small businesses with funds to provide up to 8 weeks of payroll costs, including benefits. In 2021, the PPP provided 6.7 million loans worth more than $277.7 billion. In 2020 and 2021, PPP provided a total of 11.8 million loans worth more than $799.8 billion.†

Page 274: “Table 19–4. Summary of Federal Direct Loans and Loan Guarantees1 … 1 As authorized by statute, this table includes … activity with Federal Reserve 13(3) lending facilities authorized by the 2020 CARES Act.”†

Pages 212–223: “Table 14-2. Federal Grants to State and Local Governments—Budget Authority and Outlays … General Government‡ … Coronavirus Relief Fund§”

NOTES:

[39] Report: “Fiscal Year 2023 Historical Tables: Budget of the U.S. Government.” White House Office of Management and Budget, March 2022. <www.whitehouse.gov>

“Table 3.1—Outlays by Superfunction and Function: 1940–2027” (<www.whitehouse.gov>)

“In millions of dollars … Human resources … 2021 [=] 4,807,912”

NOTE: Credit for bringing this measure to the attention of Just Facts belongs to Jodie Carroll of Vote Facts (<www.votefacts.org>).

[40] Report: “Fiscal Year 2023 Historical Tables: Budget of the U.S. Government.” White House Office of Management and Budget, March 2022. <www.whitehouse.gov>

“Table 3.1—Outlays by Superfunction and Function: 1940–2027” (<www.whitehouse.gov>)

“As percentages of outlays … Human resources … 2021 [=] 71%”

NOTE: Credit for bringing this measure to the attention of Just Facts belongs to Jodie Carroll of Vote Facts (<www.votefacts.org>).

[41] Calculated with the dataset: “Monthly Population Estimates for the United States: April 1, 2020 to December 1, 2022.” U.S. Census Bureau, Population Division, December 2021. <www2.census.gov>

“Resident Population … July 1, 2021 [=] 331,893,745”

CALCULATION: $4,807,912,000,000 human resources / 331,893,745 people = $14,486 per person

[42] Calculated with the dataset: “Table HH-1. Households by Type: 1940 to Present.” U.S. Census Bureau, November 2021. <www.census.gov>

“(Numbers in thousands) … Total households … 2021 [=] 129,931”

CALCULATION: $4,807,912,000,000 human resources / 129,931,000 households = $37,004 per household

[43] Report: “Fiscal Year 2023 Historical Tables: Budget of the U.S. Government.” White House Office of Management and Budget, March 2022. <www.whitehouse.gov>

“Table 3.1—Outlays by Superfunction and Function: 1940–2027” (<www.whitehouse.gov>)

“As percentages of GDP … Human resources … 2021 [=] 22%”

[44] Article: “Great Depression.” By Richard H. Pells and Christina D. Romer. Encyclopedia Britannica, 1998. <www.britannica.com>

“Great Depression, worldwide economic downturn that began in 1929 and lasted until about 1939. It was the longest and most severe depression ever experienced by the industrialized Western world, sparking fundamental changes in economic institutions, macroeconomic policy, and economic theory.”

[45] Report: “Fiscal Year 2023 Historical Tables: Budget of the U.S. Government.” White House Office of Management and Budget, March 2022. <www.whitehouse.gov>

“Table 3.1—Outlays by Superfunction and Function: 1940–2027” (<www.whitehouse.gov>)

NOTE: An Excel file containing the data is available upon request.

[46] Dataset: “Table 3.16. Government Current Expenditures by Function [Billions of Dollars].” U.S. Bureau of Economic Analysis. Last revised October 29, 2021. <apps.bea.gov>

Housing and community services

Health

Recreation and culture

Education

Elementary and secondary

Higher

Libraries and other …

Income security

Disability

Retirement5

Welfare and social services

Unemployment

Other

5 Consists of social insurance funds, including old age, survivors, and disability insurance (social security), and railroad retirement. Excludes government employee retirement plans.

NOTE: The U.S. Bureau of Economic Analysis includes paycheck protection and lockdown relief funds spent during the Covid-19 pandemic within the economic affairs function. Just Facts includes these funds in its measure of social spending because these are income security benefits that give “businesses the resources they need to maintain their payroll, hire back employees who may have been laid off, and cover applicable overhead.” [Webpage: “Paycheck Protection Program.” U.S. Department of the Treasury. Accessed June 8, 2022 at <home.treasury.gov>]

[47] Email from the U.S. Bureau of Economic Analysis to Just Facts, September 6, 2018.

With regard to Table 3.12 [Government Social Benefits], most tax policies and “tax preferences” affect NIPA [National Income and Product Accounts] estimates only by how they affect tax receipts. For example, the tax exclusion for employer-provided health insurance would show up in the NIPAs as lower taxes received from businesses. Only refundable personal tax credits are treated differently—we classify the full amount of these credits as social benefits, not as a reduction in tax receipts.

[48] Report: “Overview of the Federal Tax System in 2022.” By Molly F. Sherlock and Donald J. Marples. Congressional Research Service. Updated June 8, 2022. <sgp.fas.org>

Page 8: “If a tax credit is refundable, and the credit amount exceeds tax liability, a taxpayer receives the credit (or a portion of the credit) as a refund. … Some [tax] credits are phased out as income rises to limit or eliminate benefits for higher-income taxpayers.”

[49] Report: “Preview of the 2015 Annual Revision of the National Income and Product Accounts.” By Stephanie H. McCulla and Shelly Smith. U.S. Bureau of Economic Analysis, June 2015. <apps.bea.gov>

Page 2:

Federal Refundable Tax Credits

Federal income tax credits allow taxpayers who meet certain eligibility criteria to reduce the amount they are required to pay in federal income taxes. A tax credit is considered to be “refundable” if any excess of the tax credit over a taxpayer’s total tax liability is paid to the taxpayer as a refund. In contrast, tax credits are considered to be “nonrefundable” if taxpayers can only claim the credit up to the amount of their tax liability.1 Examples of refundable tax credits include the earned income tax credit and the temporary “Making Work Pay” tax credit (see table C).

|

Table C. Federal Refundable Tax Credit Programs |

|

|

Major Programs |

Program Dates |

|

Earned Income Tax Credit |

1975–present |

|

Additional Child Tax Credit |

1998–present |

|

2008 Economic Stimulus Payments |

2008 |

|

American Opportunity Tax Credit |

2009–present |

|

Making Work Pay Tax Credit |

2010–2011 |

|

Health Insurance Premium Assistance Credits |

2014–present |

Current treatment. In the NIPAs [national income and product accounts], the portion of refundable tax credits that is not directly paid to taxpayers as refunds (that is, the amount up to, but not exceeding, the total liability) is recorded as a reduction in the income taxes paid by persons to the federal government, and the portion that is paid to taxpayers as refunds (that is, any excess of the credit over the liability) is recorded as a government social benefit. This treatment provides an accurate picture of actual tax revenues and payments, but it obscures the full costs and benefits of government tax policies; that is, households not only receive the amount by which tax credits exceed their tax liabilities—but they are also relieved of the associated liabilities. Similarly, the government not only pays the refunds, but it also relinquishes its claim on the associated tax liabilities.

New treatment. As part of this annual revision, the NIPAs will record the full value of the liabilities and the credits associated with refundable tax credit programs administered by the federal government in the accounts for personal income and outlays and for federal government receipts and expenditures.2 This change will improve the consistency of the NIPAs with the System of National Accounts 2008, the international guidelines for national economic accounts, which recommends that the total value of refundable tax credits, not just the amount paid to persons, be recognized as a transfer from the government to the household sector.3 As a result, estimates of federal government social benefit payments to persons will be revised up to reflect the total amount of the refundable tax credits, and estimates of personal current taxes paid to the federal government will be revised up by an equal amount to reflect the total tax liability of taxpayers (which does not include the refunds).

[50] Report: “Estimates of Federal Tax Expenditures.” Joint Committee on Taxation, March 14, 1978. <www.jct.gov>

Pages 1–2:

The Concept of Tax Expenditures

Tax expenditure data are intended to show the cost to the Federal Government, in terms of revenues it has foregone, from tax provisions that either have been enacted as incentives for the private sector of the economy or have that effect even though initially having a different objective. The tax incentives usually are designed to encourage certain kinds of economic behavior as an alternative to employing direct expenditures or loan programs to achieve the same or similar objectives. These provisions take the form of exclusions, deductions, credits, preferential tax rates, or deferrals of tax liability. Tax expenditures also are analogous to uncontrolled expenditures made through individual entitlement programs because the taxpayer who can meet the criteria specified in the Internal Revenue Code may use the provision indefinitely without any further action by the Federal Government. This is possible because provisions in the Internal Revenue Code rarely have expiration dates that would require specific congressional action to continue the availability of the tax provision. For many provisions, the revenue loss is determined by the taxpayer’s level of income and his tax rate bracket. From the viewpoint of the budget process, fiscal policy and the allocation of resources, uncontrollable outlays or receipts restrict the range of adjustments that can be made in public policy. One of the initial purposes of the enumeration of tax expenditures was to provide Congress with the information it would need to select between a tax or an outlay approach to accomplish a goal of public policy.

Pages 4–5: